European Brand Institute

Quantifying Digital Brand Value

Brand

service line

Digital Due Diligence

Digital Brand Valuation

Digital Brand Strength Assessment

Digital Integration Index Assessment

Digital Brand Growth Assessment

Cross-Market Benchmarking

Executive Reporting & Strategic Advisory

The Case

When the European Brand Institute (EBI) prepared its annual brand valuation publication, one question stood at the centre of the conversation:

How much of a brand’s value is truly driven by digital?

EBI, a Vienna-based independent expert organisation and UNIDO partner specialising in brand and intangible asset valuation, has long been recognised for its rigorous methodology and ISO-based standards. Yet as markets become increasingly shaped by online visibility, digital engagement, and platform-driven ecosystems, traditional brand valuation needed an additional lens.

This is where our partnership began.

Cognitive Creators and EBI joined forces to complement classical brand valuation with a structured, monetised calculation of Digital Brand Value (DBV) across Austria, Germany, and Switzerland (DACH region). The goal was not to replace established valuation frameworks but to enrich them with measurable digital indicators and provide executives with a clearer view of future readiness.

The Solution

Our collaboration was built on complementary expertise:

EBI: long-standing authority in brand valuation and certification.

Cognitive Creators: a digital advisory specialising in measuring how companies create value through their digital ecosystems. Through our Digital Due Diligence methodology, we analyse a company’s digital footprint (such as online visibility, website performance, digital engagement, brand sentiment, conversion efficiency) to understand how digital channels contribute to brand performance and business outcomes. By benchmarking these signals across markets and competitors, we translate digital performance indicators into measurable brand impact.

Within the partnership, Cognitive Creators calculated the Digital Brand Value (DBV) of top companies in the DACH region using a proprietary methodology structured around four core pillars:

- Digital Brand Strength (DBS): A relative performance score measuring the strength of a brand’s digital presence compared to peers, based on indicators such as search visibility, website performance, online engagement, and brand sentiment.

- Digital Brand Growth (DBG): A relative momentum score measuring the pace of a brand’s digital expansion compared to peers, based on changes in digital visibility, engagement, sentiment, and audience reach over time.

- Digital Integration Index (DII): A relative maturity index (0-100) indicating the extent to which a company’s brand value is supported by digital channels and digital customer experiences. Lower scores suggest value creation driven mainly by traditional channels, while higher scores indicate stronger digital integration in the brand ecosystem.

- Digital Brand Value (DBV): Digital Brand Value (DBV) is the financial value generated by a brand’s measurable digital presence and digital performance.

Why It Mattered

Digital transformation is no longer about launching a new app or improving AIO visibility. It is about how deeply digital capabilities are integrated into the value creation model of a company.

The DACH analysis revealed distinct national patterns:

- Germany leads in total brand value (€239.6B for Top 10) and digital brand value (€37.7B), yet digital share represents 15.7% of total brand value - suggesting strong industrial heritage with partial digitalisation.

- Austria, while smaller in absolute scale (€39.1B total brand value for Top 10), shows the highest relative digital intensity, with 20.3% digital share - indicating agile integration of digital channels.

- Switzerland combines financial trust and global reach (€171.1B total brand value) with a 12.5% digital share, reflecting strength in traditionally conservative sectors and further digital potential.

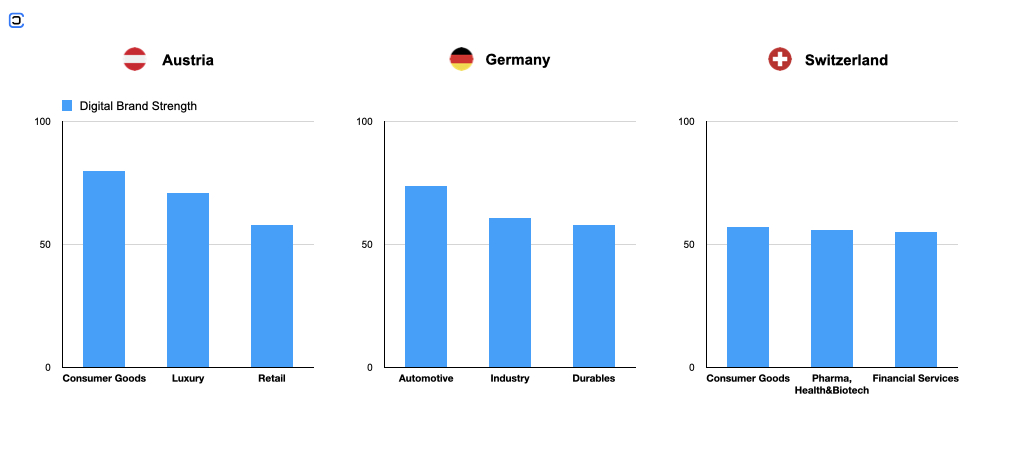

At sector level:

- Germany demonstrates digitally mature ecosystems in Automotive and Industrial sector (secondary and goods-producing sector).

- Austria shows strong digital brand strength in Consumer Goods and Luxury.

- Switzerland presents a balanced presence across Consumer Goods, Pharma/Health, and Financial Services, with room for deeper digital integration.